Ask any established cannabis entrepreneur or operator to name their most challenging financial hurdles, and it’s likely they’ll respond with “banking relationships” and #1excludeGlossary.

Ask any established cannabis entrepreneur or operator to name their most challenging financial hurdles, and it’s likely they’ll respond with “banking relationships” and #1excludeGlossary.

Most cannabis operations are running all-cash businesses because mainstream, national banking institutions are not willing to support a federally illegal industry. A SMALL number of state-chartered banks and credit unions have offered financial services to compliant operations, but establishing these relationships continues to be a significant challenge for operators.

An equally frustrating financial challenge is IRS Tax Code 280E, which states that “no deduction or credit shall be allowed in running a business that consists of trafficking a controlled substance.” This archaic code impacts cannabis businesses across the nation, causing unnecessary fiscal and operational stress.

By understanding the history of the code, and best practices related to tax management and cannabis accounting, you can avoid 280E pitfalls and approach it with confidence.

280E History

Federally, cannabis is considered a Schedule 1 Controlled Substance alongside Heroin, LSD, and Ecstasy. In 1982, at the height of drug hysteria and increased drug-related incarceration rates, Congress created Section 280E of the Internal Revenue Code (IRC).

Federally, cannabis is considered a Schedule 1 Controlled Substance alongside Heroin, LSD, and Ecstasy. In 1982, at the height of drug hysteria and increased drug-related incarceration rates, Congress created Section 280E of the Internal Revenue Code (IRC).

This was in reaction to a court case in which a convicted cocaine trafficker asserted his right under federal tax law to deduct ordinary business expenses (such as rent, advertising, and employee salaries), Congress created 280E to prevent other drug dealers from following suit (source).

#6excludeGlossary to today; legitimate, state-legal businesses are building compliant operations to provide access to medical cannabis and adult-use cannabis, yet still have to face the BURDEN of paying taxes for normal business expenses.

What is IRS Code 280E?

Here’s a summary of 280E and what it means for cannabis businesses today:

Here’s a summary of 280E and what it means for cannabis businesses today:

- Intended to prevent drug dealers from claiming tax deductions for their business expenses

- Interpreted to include state-legal cannabis businesses

- Reduction of deductions results in increased taxable income

- Cannabis companies face higher federal tax rates: 40 – 80% versus 21% corporate tax

From an industry outsider’s perspective, it may seem like the businesses of legal cannabis are swimming in profits. However, this code is making a huge portion of dispensary revenues susceptible to tax, hindering these licensed businesses from being able to invest in building improvements, pay raises, benefits, operational expansions, giving back to the community, and so much more.

Cannabis Verticals Affected By 280E

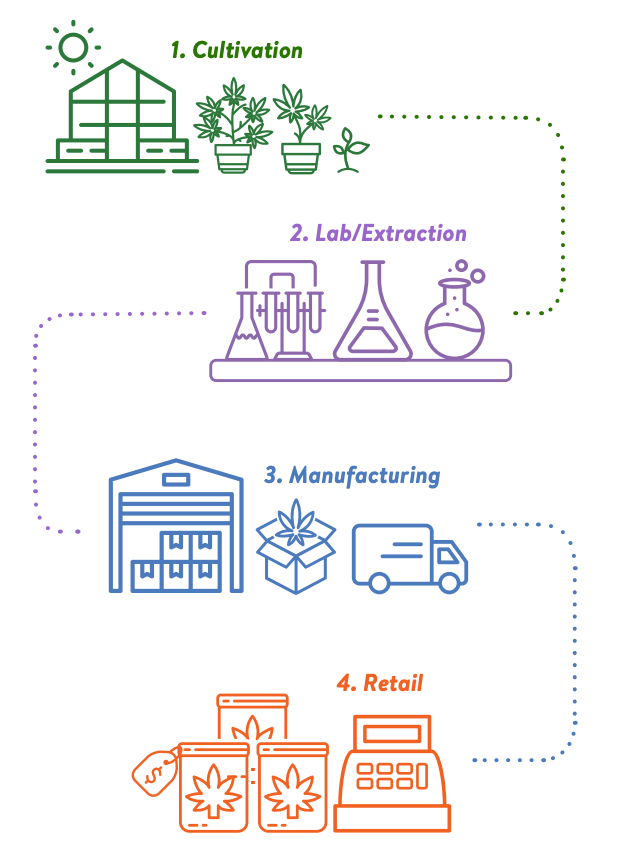

Since 280E is directly related to the selling or the “trafficking” of cannabis-related products, it impacts retail operations the most. However, it is important to understand the entire “Seed-to-Sale” concept and overall structure to truly understand how your business will be affected. Cannabis verticals are categorized by these functions:

Since 280E is directly related to the selling or the “trafficking” of cannabis-related products, it impacts retail operations the most. However, it is important to understand the entire “Seed-to-Sale” concept and overall structure to truly understand how your business will be affected. Cannabis verticals are categorized by these functions:

- Cultivation / Grow

- Processing / Infusions / Extractions

- Retail Dispensary

- Vertically Integrated: Licensed in every area of the cannabis lifecycle, meaning you grow, produce, and sell your products.

If you wholesale product to another vendor or retailer, this is considered trafficking, and you can be subject to 280E. When calculating deductions, having a DISTINCT separation between these verticals and seed-to-sale job functions will be vital.

280E Tax Deductions & Deductible Expenses

Identifying whether deductions can be allocated as Cost of Goods Sold (COGS) can significantly minimize the tax impact of 280E on your cannabis business. If you cultivate, produce, extract, or infuse cannabis, COGS related to the growth and production of goods that are then wholesaled by your business, are potentially subject to 280E. The bulk of activities of cultivation or extraction within a vertically-integrated operation can be considered COGS and transportation and delivery may be considered non-deductible COGS.

280E COGS Types

Careful analysis with a cannabis accountant must be done to ensure you’re compiling these deductions while remaining compliant. Here is a suggested list of the types of 280E deductible labor COGS you can leverage:

Careful analysis with a cannabis accountant must be done to ensure you’re compiling these deductions while remaining compliant. Here is a suggested list of the types of 280E deductible labor COGS you can leverage:

Cannabis cultivators may also claim deductions for:

- Raw materials and supplies (seeds, clones, fertilizer)

- Indirect product costs, such as equipment maintenance, utilities used to grow cannabis, supervisory wages, and costs of quality control and inspection

As a stand-alone dispensary, COGS are limited to the cost of the product and the costs of acquiring the merchandise, including the transportation costs to purchase the wholesale cannabis. You may also CLAIM deductions for electric bills for designated inventory areas.

From that point on, virtually everything else is subject to 280E scrutiny in the retail environment. Keep an accurate chart of accounts so you can properly code direct and indirect costs in real time. All operators should work with certified cannabis law, tax, and accounting experts to manage 280E.

Keeping 280E Records

Accurate recordkeeping will save hours of time and costly mistakes when managing 280E deductions. Ensure you have electronic methods to manage documentation for your workforce, inventory, spending, etc. Report all cash transactions, including:

Accurate recordkeeping will save hours of time and costly mistakes when managing 280E deductions. Ensure you have electronic methods to manage documentation for your workforce, inventory, spending, etc. Report all cash transactions, including:

Your accountant will work to designate specific COGS and advise you to record detailed COGS deductions and what may or may not qualify. Every step you can take to leverage 280E best practices and authenticate labor hours, COGS, and spending will help offset unnecessary tax overpayments.

280E Accounting Overview

When it comes to cannabis accounting 101 and your overall accounting strategy, the inventory accounting method typically provides the most benefits. This method requires producers to capitalize on costs that are both incident to and necessary for production or manufacturing operations or processes.

When it comes to cannabis accounting 101 and your overall accounting strategy, the inventory accounting method typically provides the most benefits. This method requires producers to capitalize on costs that are both incident to and necessary for production or manufacturing operations or processes.

Work with a Certified Public Accountant (CPA) to determine the proper inventory capitalization and valuation methods, allocation of expenses, and their impact on the Cost of Goods Sold under Sec. 471.

Additionally, ensure you fully understand how to avoid money-laundering behaviors, especially as a cannabis operation with multiple Employer Identification Numbers (EINs) or as an all-cash business. Some of the behaviors you will want to avoid may include:

- Structuring cash-in transactions

- Using multiple locations to purchase negotiable instruments

- Trying to withhold or refuse to provide the information needed for Currency Transaction Report (CTR) or Form 8300

- Providing false information for CTR or Form 8300

- Volunteering information to financial institutions regarding cannabis-related businesses as a source of income

- Providing money to a financial institution that has a cannabis odor

Potential outcomes for violations related to money laundering could include the costs of investigations, losing your cannabis license, civil litigation, or even jail time. Generally, tax audits for cannabis companies are not a matter of if, but a matter of when, so establish clear and concise accounting processes to ensure you’re prepared.

280E Compliance Cannabis Tracking Software

![]() Accurate labor tracking through cost centers enables managers to streamline identifying 280E workforce deductions, which can significantly IMPACT the negative effects of the code.

Accurate labor tracking through cost centers enables managers to streamline identifying 280E workforce deductions, which can significantly IMPACT the negative effects of the code.

For example, it’s important to track if a Dispensary Technician spends a few hours in the morning training (deductible) and then begins selling product in the afternoon (non-deductible under 280E). Utilizing employee time and attendance software for cannabis can greatly improve your ability to optimize labor deductions by providing:

- Self-service on any device employees to track tasks, jobs, and cost centers

- #23excludeGlossary labor reports and audit trails

- Easy on-screen access to compliance-related data

- Multi-format data exports for additional systems or accounting software

Unlike mainstream human capital management solutions, industry-specific cannabis Learning Management System (LMS) software and systems are built to support the complex cannabis regulatory environment and its many training intricacies.

If 280E is not managed properly, profits can erode quickly by increased tax liabilities… and in some cases, be wiped out completely. Understanding the implications of the code and partnering with experienced cannabis tax advisers is key to operating a compliant, profitable cannabis company.

Let us know what you think.